Case Study: What Credible analysts are saying on Disney (DIS) stock

Key Points

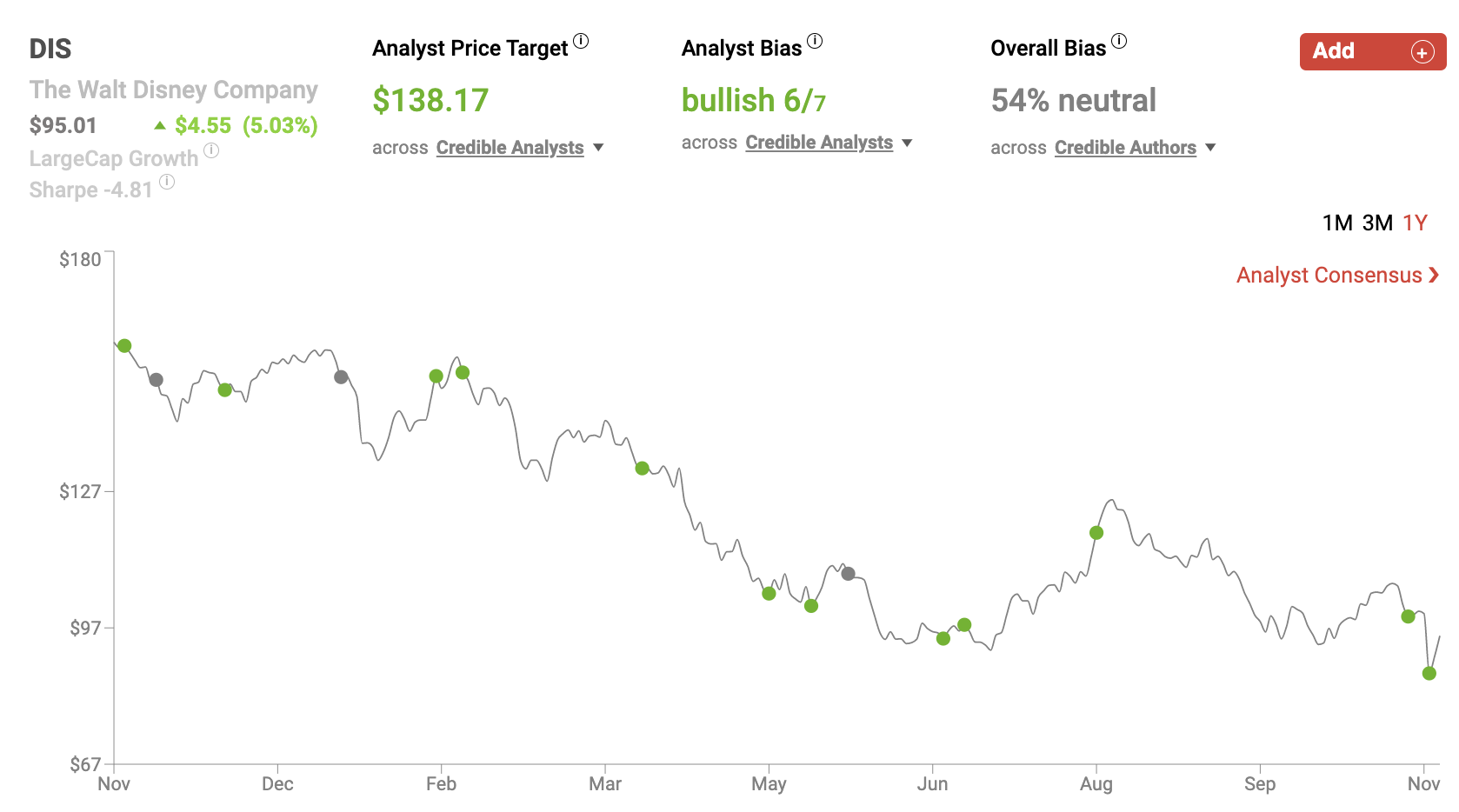

The Walt Disney Company shares sold off more than 5.5% this week. DIS shares are now down nearly 39.4% on the year, drastically underperforming the S&P 500, which is down by 16.75% during 2022 thus far.

Disney continues to invest heavily in its streaming platform and direct to consumer content; however, management doesn’t expect its Disney+ streaming service to be profitable until 2024.

Disney reported Q4 earnings this week, missing Wall Street’s estimates on both the top and bottom lines.

54% of credible authors offer a “Neutral” bias towards Disney shares. 6 out of the 7 credible Wall Street analysts believe that DIS shares are headed higher. The average price target being applied to Disney shares by credible analysts is $138.17 which implies upside potential of approximately 45.4% relative to DIS’s current share price of $95.01.

Performance

Event & Impact

Noteworthy News:

Nobias insights

Shares of the Walt Disney Company (DIS) fell by 5.54% this week, bucking the bullish trend that the broader indexes experienced. The S&P 500 rose by 5.82% this week, pushing its year-to-date performance up to -16.75%. Disney, on the other hand, is now down by 39.39% on the year, making it a drastic underperformer on the year.

Disney released its fourth quarter/full year earnings report this week. Disney missed Wall Street’s estimates on both the top and bottom lines, posting quarterly revenue of $20.15 billion, $1.29 billion below consensus, and non-GAAP earnings-per-share of $0.30, missing Wall Street’s target by $0.26.

The company highlighted its fundamental results, stating:

Revenues for the quarter and year grew 9% and 23%, respectively.

Diluted earnings per share (EPS) from continuing operations for the quarter was comparable to the prior-year quarter at $0.09. Excluding certain items(1), diluted EPS for the quarter decreased to $0.30 from $0.37 in the prior-year quarter.

Diluted EPS from continuing operations for the fiscal year ended October 1, 2022 increased to $1.75 from $1.11 in the prior year. Excluding certain items(1), diluted EPS for the year increased to $3.53 from $2.29 in the prior year.

Disney’s CEO, Bob Chapek, led off the press release with a statement: “2022 was a strong year for Disney, with some of our best storytelling yet, record results at our Parks, Experiences and Products segment, and outstanding subscriber growth at our direct-to-consumer services, which added nearly 57 million subscriptions this year for a total of more than 235 million. Our fourth quarter saw strong subscription growth with the addition of 14.6 million total subscriptions, including 12.1 million Disney+ subscribers. The rapid growth of Disney+ in just three years since launch is a direct result of our strategic decision to invest heavily in creating incredible content and rolling out the service internationally, and we expect our DTC operating losses to narrow going forward and that Disney+ will still achieve profitability in fiscal 2024, assuming we do not see a meaningful shift in the economic climate. By realigning our costs and realizing the benefits of price increases and our Disney+ ad-supported tier coming December 8, we believe we will be on the path to achieve a profitable streaming business that will drive continued growth and generate shareholder value long into the future. And as we embark on Disney’s second century in 2023, I am filled with optimism that this iconic company’s best days still lie ahead.”(2)

Looking at Disney’s operating segment performance, the company’s press release highlighted -3% revenue growth from the Disney Media and Entertainment Distribution segment and 36% revenue growth from the Disney Parks, Experiences and Products segment.

DIS Nov 2022

Disney’s media segment posted $12.75 billion of sales and Disney’s Parks segment posted $7.4 billion of sales. Disney highlighted 39% growth of Disney+ subscribers; however, the company’s average monthly revenue per subscriber fell by 10% in the U.S. and Canada market. Disney+ Core’s average monthly revenue per subscriber fell by 4% and Global Disney+ saw this same metric fall by 5%. So, while management has succeeded in growing its subscriber base, it appears to be sacrificing near-term profits for subscriber gains.

During Q4, Disney’s cash from operations fell by 4% and its free cash flow fell by 10%. Falling margins, net income, and free cash flow fueled the bear’s negativity, leading to a 10%+ sell-off following this Q4 earnings release. Yet, as Chapek said, the company still believes that Disney+ will be a profitable operation by 2024, providing optimism for bulls.

Bullish Nobias credible authors:

Dani Cook, a Nobias 4-star rated author, wrote about Disney’s recent earnings report in a bullish article at the Motley Fool this week. Cook said, “The company's fourth-quarter earnings release on Nov. 8 was a bit of a mixed bag, as its parks revenue soared, but its media segment took some concerning hits.”

Cook mentioned the threat of recession moving forward and the potential negative impact of this on Disney’s consumer-centric business model; however, she also stated, “While Disney's short-term prospects may be uncertain, the company has proven the staying power of its content and is home to some of the world's most in-demand franchises.”

Because of the experiential aspect of Disney’s business (live sports, theme parks, and cruise ships) the company experienced a lot of volatility during the pandemic. Cook highlighted this stating, “Its parks business experienced massive losses due to closures, while its streaming service Disney+ seemed to launch at the perfect time in 2019. The streaming service received a significant boost to its growth as home-bound people flocked to online entertainment platforms.”

But ultimately, she is bullish on the company because of the strength of its steaming platform. Cook said, “In three years, Disney+ has reached 164.2 million members, pushing the company's total streaming subscribers to 235.7 million, and beating Netflix's (NASDAQ: NFLX) 223.09 million.”

Therefore, she continued, “Disney+ has risen faster than any streaming service in history.” Adding color to the Disney+ and Netflix comparison, Cook wrote, “Industry founder Netflix didn't reach Disney+'s current subscriber count until 2019, 12 years after its streaming service launched in 2007. Disney has accomplished its swift streaming expansion with the draw of its incredibly potent content brands such as Marvel, Star Wars, Pixar, 20th Century Studios, and all of its franchises from Walt Disney Studios.”

But, she says, this growth hasn’t come without headaches. Cook said that Disney’s Media segment posted -91% year-over-year growth in terms of its operating income, writing, “The slump in earnings from Disney's Media and Entertainment segment was primarily driven by the company's $30 billion content spend in 2022 as it worked to grow Disney+.”

Despite the rising costs associated with building out its streaming service, Cook likes the over-the-top media space, stating that this is currently a $327 billion industry. Regarding the forward growth prospects of streaming services, Cook said, “Fortune Business Insights expects it to see a 19.9% compound annual growth rate and reach a value of $1.6 trillion by 2029.”

Cook points out that Disney has taken steps to diversify the content on Disney+ in recent years as it attempts to expand its subscriber base. And, she said, “Disney isn't done yet”. Cook said that Disney’s plans for an ad-supported version of Disney+ “still has yet to launch, which could open the door for a revenue boost in the second half of fiscal 2023.”

Ultimately, she concluded, “Disney has embarked on an expensive but promising transition to diversify its business, maximize efficiency, and grow revenue over the long term. And with a price-to-earnings ratio at 69% below what it was a year ago, Disney stock is a bargain and worth buying on the dip to hold long-term.”

Long Player, a Nobias 5-star rated author, also published a post-earnings article this week, focusing largely on the “culture wars” that Disney has been fighting in recent years. The author began their piece stating, “Disney (NYSE:DIS) long ago made a statement about inclusion and diversity that earned the ire of the state of Florida. That ire meant that a very inadequate law was passed that meant for Florida to dissolve the self-governing unit that Disney has for its business unit, the theme park. But the law never stated how to unwind decades of business deals, nor did it state how bondholders would be paid off. Paying off the bondholders is part of the bond covenants.”

Long Player noted that the strong rhetoric surrounding Disney’s culture issues had quieted in recent quarters, with investors focused instead on its post-COVID-19 rebound. “But, “ the author stated, recently “the CEO made a statement about "woke" which the news promptly carried and may well start the whole thing up again if management is not careful.”

Long Player said, “Disney got itself caught in an unfortunate situation about diversity. Right now, that discussion appears to be largely out of favor in Florida. Despite the law being passed, there's unlikely to be a material change in the situation because bondholders have a change of control as part of the bond covenant.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Long Player states that these political issues add uncertainty to Disney’s outlook moving forward, yet looking at the company’s recent results, they aren’t hurting the company’s growth. Long Player wrote, “For all the talk about characters being appropriate for families and children, the company seems to have had no problems attracting streaming customers.” They continued, “This business, however, now needs to turn from the showing loss to a profit. That may or may not be possible, given that the streaming "wars" are just getting started.”

Long Player distinguishes Disney from its media peers, stating, “Disney does have an advantage in that the other parts of the integrated company may derive enough benefits from the streaming segment so that the company does not have to report a profit. Not all competitors appear to be in the same position.”

Regarding ongoing growth prospects for Disney, Long Player said, “The acquisition of 21st Century Fox has yet to be fully exploited.” They continued, “That will likely happen in the post-pandemic period. But it could take a year or two for investors to see the results.

Acknowledging the “woke” headwinds, the author concluded, “The recovery potential far outweighs any adverse possibilities in Florida, if they even happen.”

Overall bias of Nobias Credible Analysts and Bloggers:

Looking at the opinions expressed by the credible authors and credible analysts that the Nobias algorithm tracks, there is a schism between the two communities. 54% of recent articles released by credible authors have expressed a “neutral” bias for Disney shares. However, 6 of the 7 credible Wall Street analysts that Nobias tracks believe that DIS shares are likely to rise in value.

Right now, the average price target being applied to DIS shares by credible analysts is $138.17. Relative to the stock’s current share price of $95.01, that average price target represents upside potential of approximately 45.4%.

Disclosure: Nicholas Ward is long DIS shares. Nicholas Ward wrote this article for Nobias at their request with the intention of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.